2023 Africa Tech

Venture Capital

Even more striking, half of the investors disappeared from the market and those who stayed were less active.

It’s clearly a good time to pause, take stock of the ecosystem and ponder where it might go next.

Looking all the way back to our first report published at the end of 2016, we can only marvel at the journey from then to 2023. Even after the correction, the ecosystem has grown by nearly 10x in transactions as well as in amounts invested. It’s a total of nearly 3,000 rounds and $20B over the last 10 years, 68% of it in the last 3 years. We have seen VC activity spread from a handful of countries to 38. Even though the top 4 markets have stayed dominant, entrepreneurs almost everywhere are getting more exposed to investors and a chance to access resources to build innovative companies. In total nearly 3,000 investors have been active on the continent over this 10 year period, committing to these entrepreneurs and their vision.

We have witnessed the emergence of a full-blown Africa tech VC ecosystem. And what a rocky infancy for this ecosystem: it went through COVID, the 2021 VC craze, and the SVB collapse. Each of these forced all the players to adapt, learn, and build new mechanisms and safeguards.

So here we are with another crisis. Another occasion to once again adjust, learn, come out stronger.

And some learnings have started crystallizing already. As the influx of capital dried up, companies strived to control cash burn. Founders had to learn the importance of being “default alive”, i.e. simply not dying if the next fundraising target was missed. Board meetings are focusing on growing in a more sustainable way, discussing paths to profitability. Many had to learn in dire circumstances how to navigate the downside scenarios: down rounds, lay-offs, bankruptcy filings,… And many of these learnings will continue to apply when the crisis is behind us, and a new cycle of growth starts.

But amidst all this turmoil the fundamental forces propelling the emergence of this tech ecosystem will continue to shape its near future: growing economies, accelerating tech penetration and an entrepreneurial talent pool that is getting deeper and stronger.

As a result, there are a few predictions we can make with confidence: founders who have secured their businesses against the headwinds will see room for growth and less competition; investors who are committed to this region, those who stay the course, will find better opportunities; the ecosystem will keep growing.

We are looking forward to chronicling new aspects of this growth in the Partech Africa Report.

Topline Deals and Volumes

African VC investments experienced a significant downturn

with a 46% decline in total funding and, for the first time in 8 years

of reporting, a 28% decline in deal count.

While in 2022 this region stood out against the global downturn,

in 2023 the African tech sector saw a larger decline

than the global trend despite a display of resilience on the debt side.

In 2023, the global venture capital ecosystem faced considerable challenges, leading to significant changes in investment patterns. Global equity funding experienced a sharp decline of 38% YoY to $285B1 while venture debt saw a more modest decrease of 5% to $59.2B2.

African tech was not immune to these macroeconomic headwinds, and the year ended with the region securing just over half of the funding it had achieved in 2022:

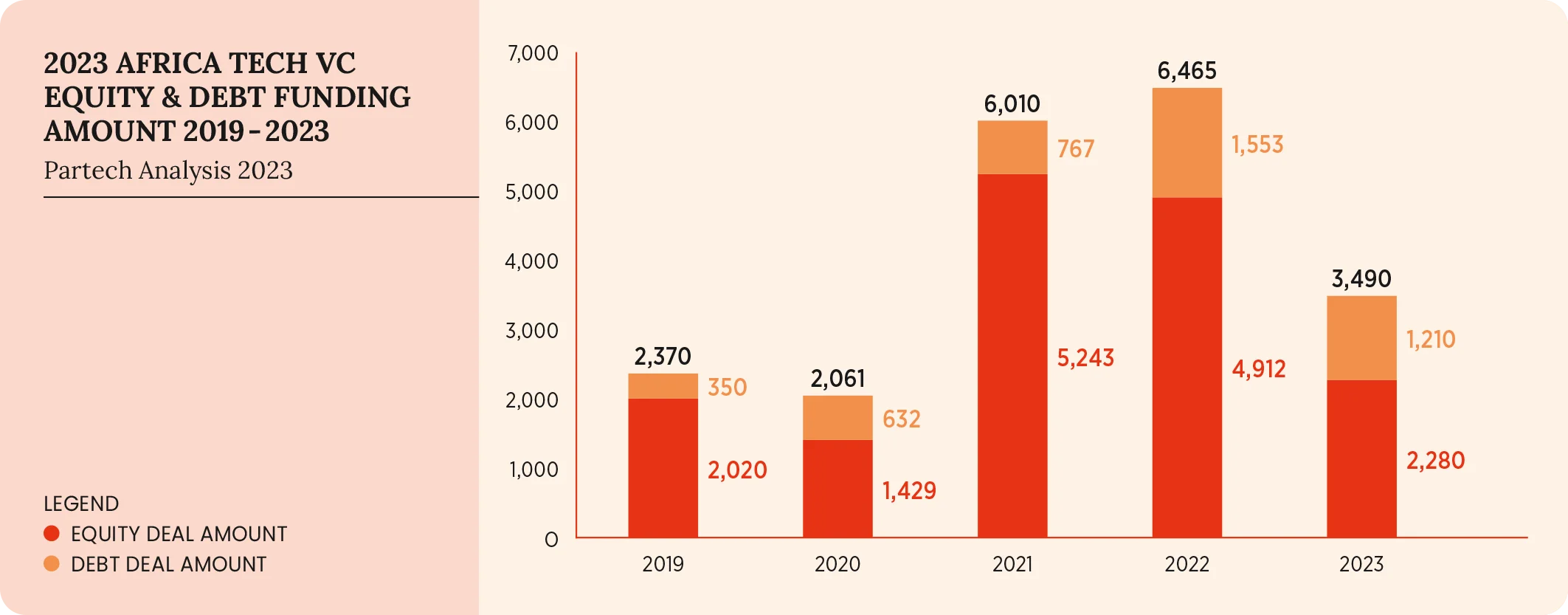

- Total funding, including both equity and debt, fell by 46% year-over-year, from $6.5B to $3.5B.

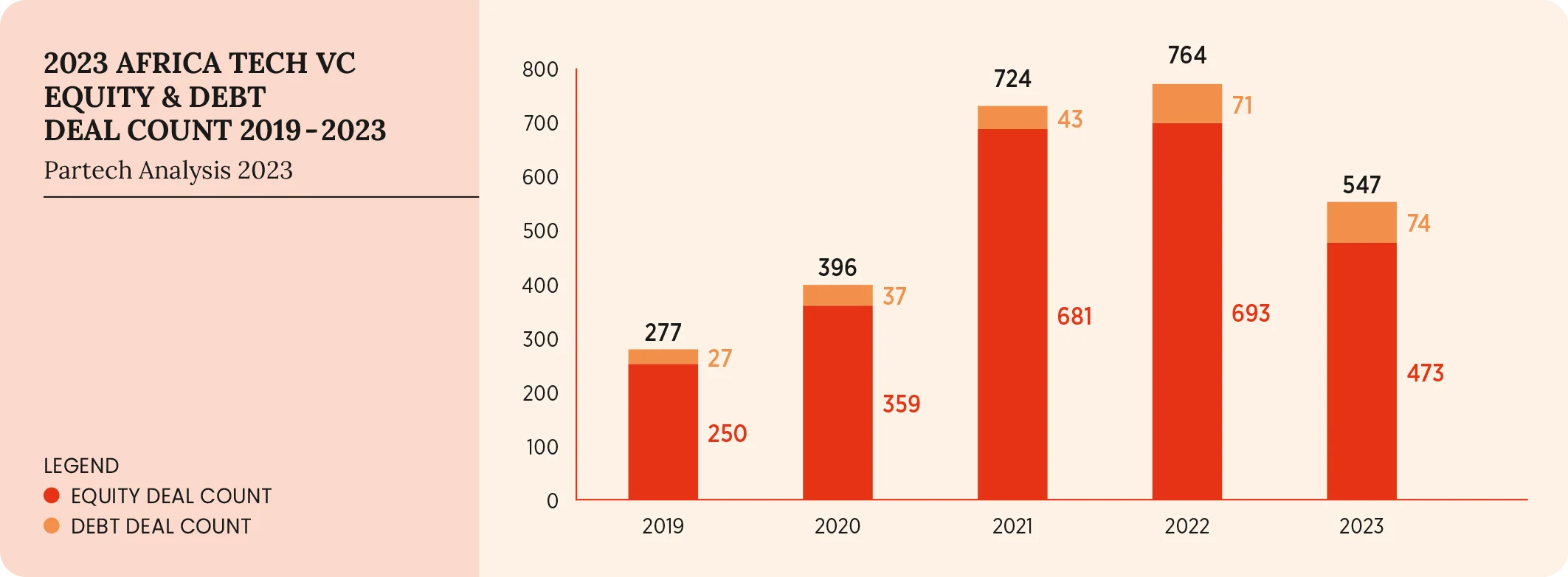

- Even more striking, the number of deals completed also saw a significant reduction, dropping by 28% from 764 to 547 deals, marking for the first time, in the 10+ years of data we have, a decline in deal count in this fast-growing ecosystem.

Beyond the known challenges linked to the global macroeconomic environment (i.e., high interest rates, currency devaluation, inflation, layoffs), two key factors contributed to this contraction in funding:

- Conservative Capital Raising: Faced with strong valuation decline and stronger requirements on their economics, many startups focused on cash efficiency over fundraising.

- Investor Withdrawal from the Market: Compared to last year, the number of investors that participated in funding rounds in Africa in 2023 decreased by 50%. There was a major decline in participation from major institutional funds, who generally drive the larger rounds. For instance, we noted only 1 equity and 3 debt megadeals in 2023 (i.e., above $100M), compared to 7 equity and 4 d ebt megadeals in 2022.

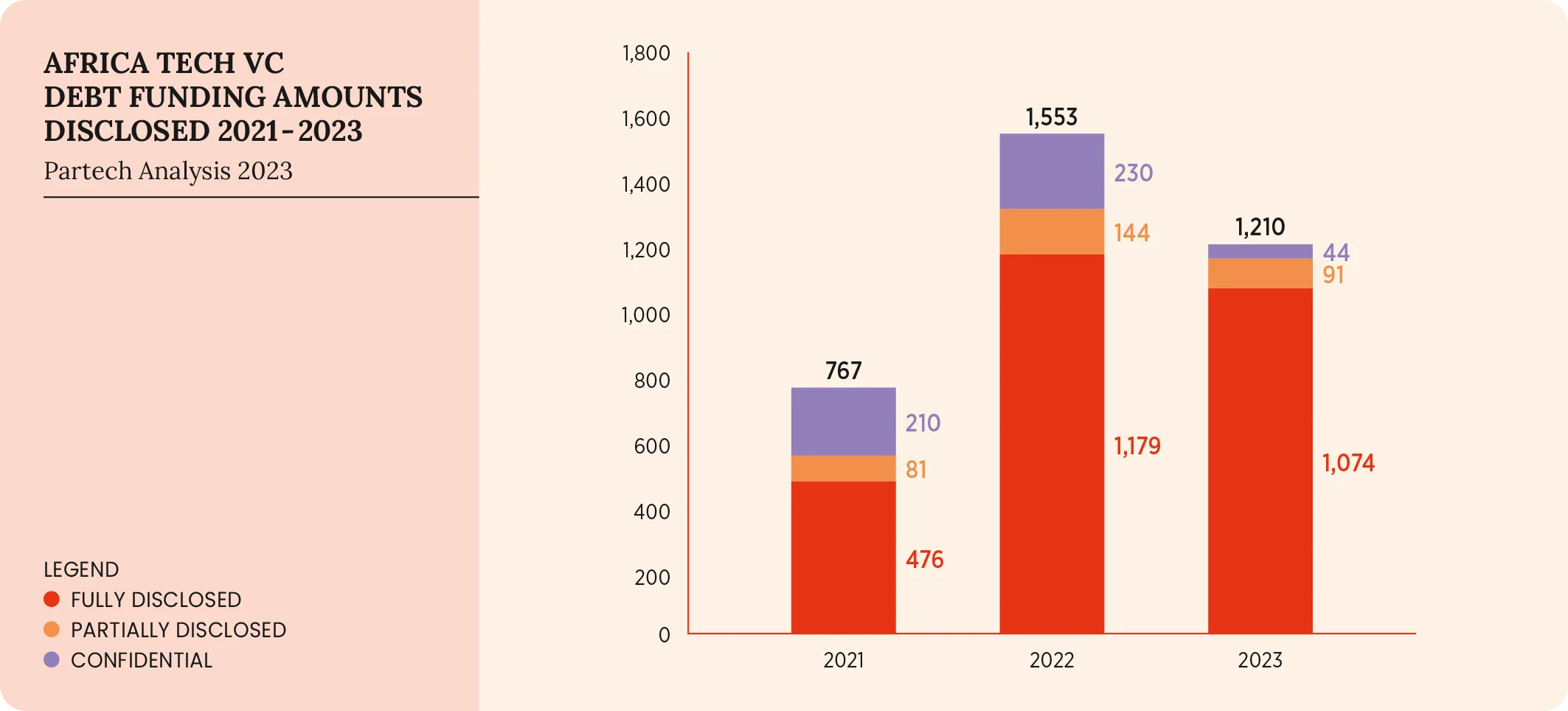

Despite this downward trend, a standout in this landscape was the resilience of debt deals, which continued to be made available to African tech startups. The number of deals saw a modest increase from 71 in 2022 to 74 in 2023, and while there was a 22% decrease in the amount raised, from $1.6B in 2022 to $1.2B in 2023, it was less severe compared to the overall funding downturn notably thanks to 8 deals above $50M (vs. 7 in 2022).

To put this overall downturn in perspective, it is crucial to recognize that:

- The decline in funding is occurring in the context of a global downturn which appears to be hitting the African ecosystem with a delay of roughly two quarters.

- Other emerging markets have been experiencing similar downward trends in VC funding, in the case of Latin America and Southeast Asia, on a larger scale.

- Despite the downturn, current levels of funding still present a significant growth over the past five years – nearly doubling the pre-2021 figures.

Equity Breakdown

Download the full report to read this section.

Debt Breakdown

Download the full report to read this section.

Methodology & Disclosure

Scope: We report on fundraising for African tech and digital startups, specifically venture capital equity and debt deals above $200K.

Methodology and disclosures:

We include only equity or debt rounds that are $200K or above. This means our focus is on Late Seed (Seed+) to Growth stage equity & debt rounds.

Example: South African LeaseSurance’s $161K Seed round is not counted.

Geographic Focus:

Our coverage is limited to African startups, defined as those whose primary market (by operations and/or revenues) is in Africa. Companies that expand globally are still considered African if their primary market remains on the continent.

Example: Bitget’s $10M Series B round, despite its Seychelles HQ, is not counted as its primary business is not in Africa.

Exclusions:

We exclude all non-equity and non-debt financial instruments: grants, awards, prizes, Initial Coin Offerings (ICOs), non-equity/technical assistance, post-IPO activities, private investment in public equity (PIPE), securitization and all M&A deals.

Examples:

- Egyptian company MNT-Halan’s $130M raise in securitized bonds is not counted.

- South African company e4’s $54M acquisition is not counted.

- Kenyan company Maisha Meds’ $5.25M grant is not counted.

Our approach is designed to capture a substantial portion of investment activities that influence the market, with a particular emphasis on the African tech and venture capital scene. However, it is crucial to acknowledge that despite our best efforts, the report might not capture every aspect of the investment activities within our defined scope. Due to the confidential nature of some deals, there could be instances of undisclosed transactions or partial information on certain deals. Our primary objective continues to be offering a realistic and practical picture of the state and progression of the African Tech VC ecosystem, drawing upon publicly available data and insights gathered from our network.

We extend our heartfelt thanks to everyone who responded to our data gathering requests, as their contributions have been invaluable in shaping our understanding.

DATA SOURCES AND TRANSPARENCY

Our data collection process categorizes deals into three disclosure levels:

- Fully Disclosed:

Deals announced publicly through press releases or platforms like CrunchBase, Tracxn, PitchBook, etc., with details on series, round size, and investors. - Partially disclosed:

Deals with public announcements but lacking details like round size. We supplement this data by engaging with our network of founders and investors. - Confidential:

Deals not disclosed publicly. We gather this data through direct engagements under confidentiality agreements.

The below will provide aggregate metadata on the level of disclosure in our database entries for equity deals, debt deals, and both debt and equity combined.

ALL DEALS

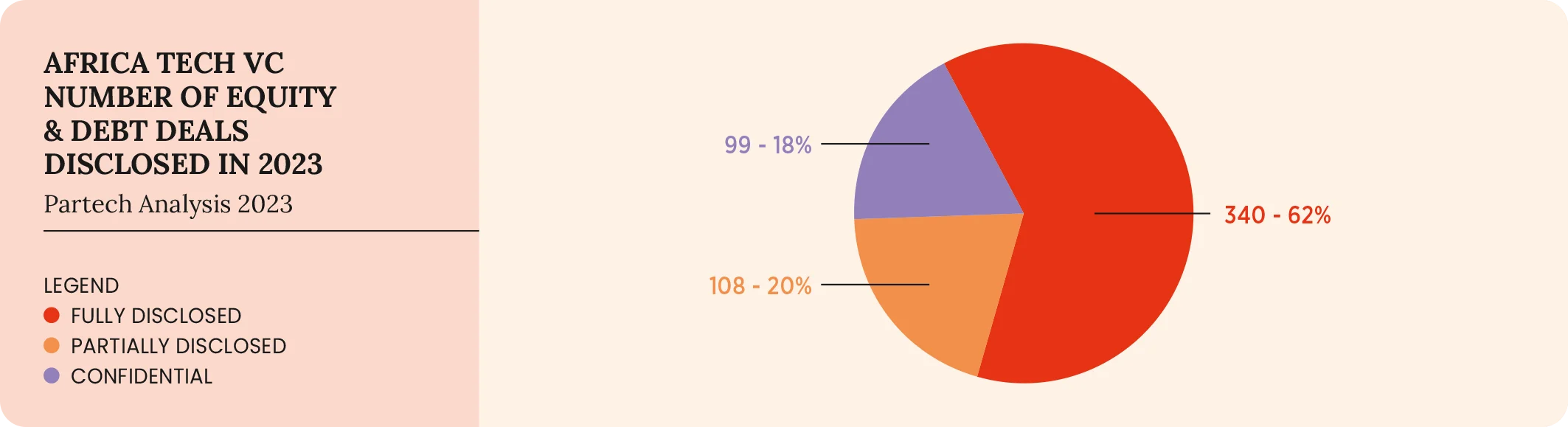

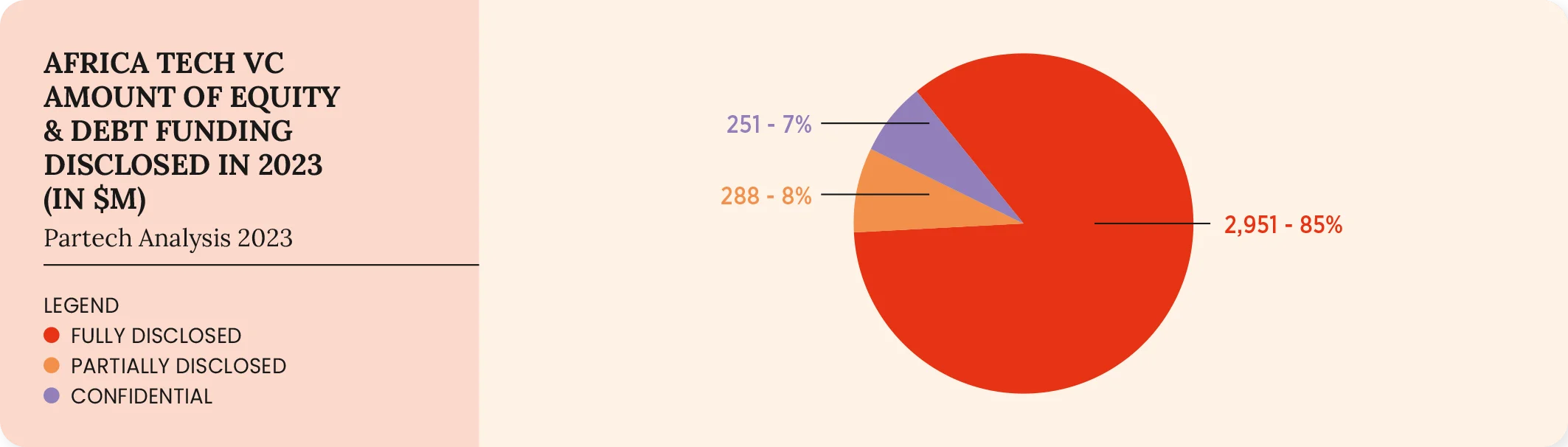

Looking at all equity and debt deals, the fully disclosed and partially disclosed deals represent 340 transactions out of 547 or 62% of the total deal count, translating into $3B out of $3.5B or 85% of the total funding.

DISCLOSURE OF EQUITY DEALS

KEY FIGURES

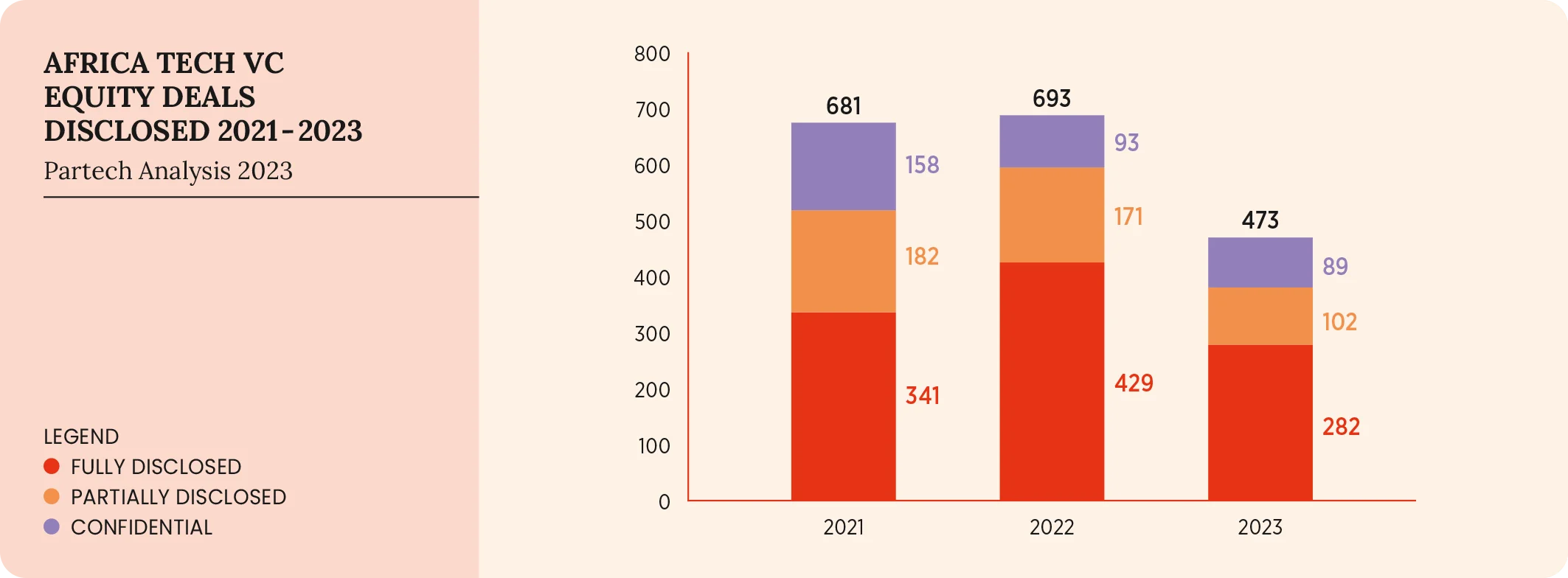

FULLY DISCLOSED: 60% of deals have been fully disclosed in 2023 (282 deals), representing

82% of equity funding amount.

PARTIALLY DISCLOSED: 22% of deals have been partially disclosed in 2023 (102 deals), representing 9% of equity funding compared to 7% in 2022.

CONFIDENTIAL: 19% of deals were kept entirely confidential, significantly higher than 2022 (10%).

In analyzing the disclosure trends, equity and debt deals have followed a relatively consistent pattern over the course of the year. However, notable differences emerge when breaking down the data by the type of funding instrument.

Equity deals in 2023 have experienced a slight decline in the proportion of fully disclosed transactions: down to 60% (comprising 282 deals), from 61% in 2022. In contrast, the number of confidential deals grew significantly, from 13% in the previous year to 19% in 2023.

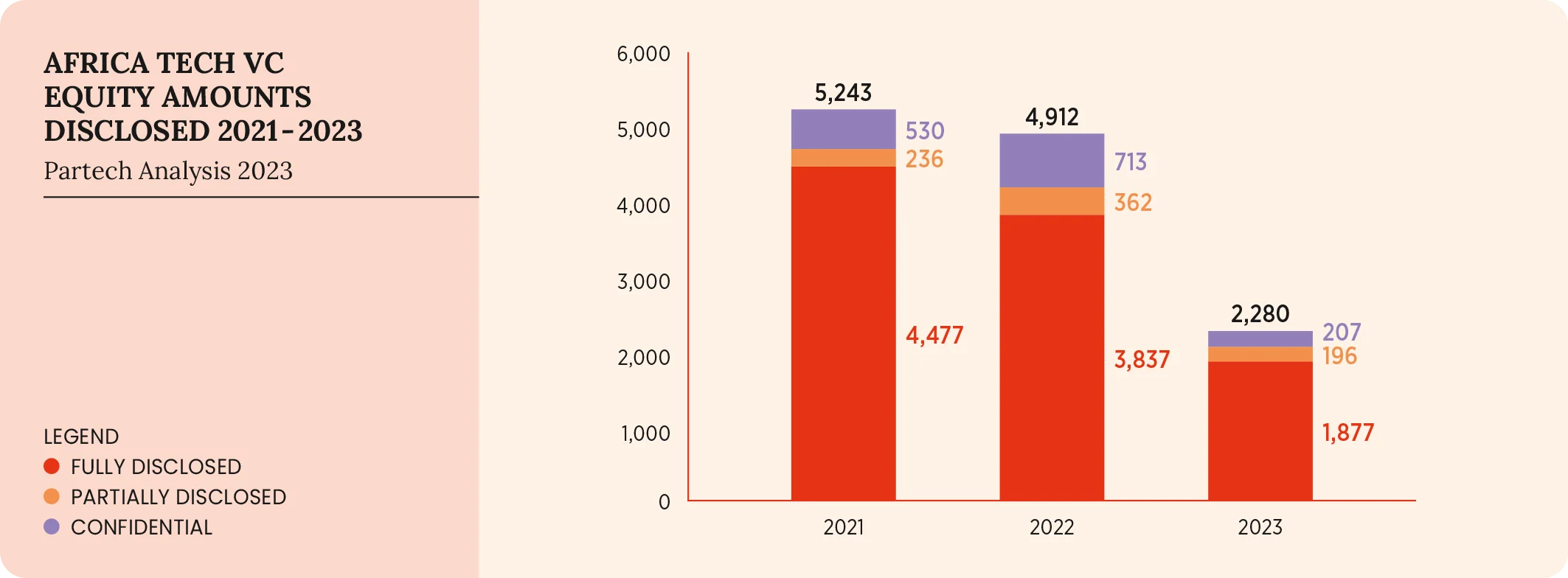

This shift in disclosure trends is further nuanced when considering the actual funding amounts involved. Despite the growing number of confidential deals, 82% of the total equity funding for 2023 has been fully disclosed, an increase from 78% in 2022. Partially disclosed deals have also witnessed a marginal rise in their share of the funding, climbing from 7% in 2022 to 9% in 2023.

Conversely, the funding amounts associated with confidential deals have not mirrored this upward trend; they decreased slightly from 15% in 2022, to 9% in 2023.

A deeper dive into the underlying data reveals a distinct trend in the stages of deals and their disclosure status. Approximately three-quarters of later- stage deals, specifically those in Series B and Growth stages, are typically announced publicly. On the other hand, early-stage deals, namely those in the Seed and Series A stages, have only about half of their transactions fully disclosed. This difference in disclosure rates between smaller early-stage deals and larger later-stage deals accounts for the disproportionate representation of fully disclosed transactions in terms of funding amounts, as opposed to the actual number of deals.

These trends and insights highlight the evolving nature of disclosure practices in the African tech venture capital space, particularly in a tough macroeconomic environment that has seen multiple down-rounds, reflecting a complex relationship between the stage of investment and the preference for confidentiality in deal-making.

DISCLOSURE OF DEBT DEALS

KEY FIGURES

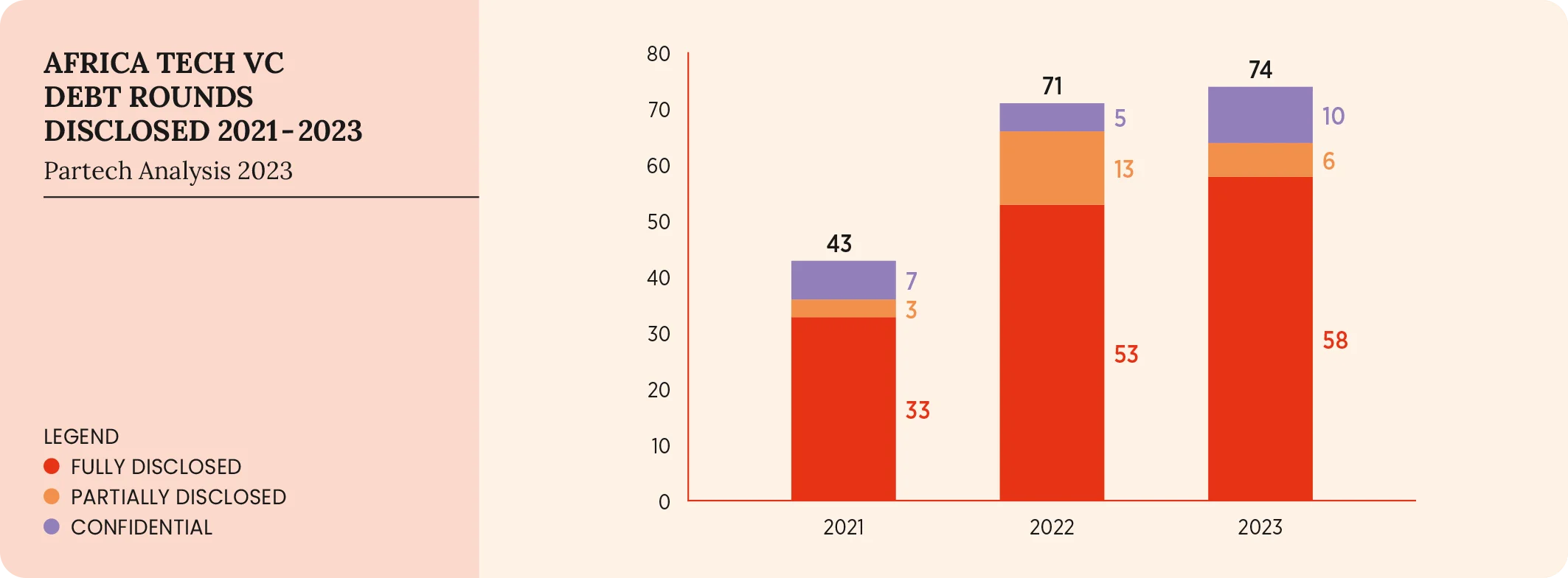

FULLY DISCLOSED: 78% of the deals (58 deals) were fully disclosed in 2023. This represents 89% of debt funding.

PARTIALLY DISCLOSED: 8% of deals have been partially disclosed in 2023 for both deal count and funding amount.

CONFIDENTIAL: 14% of deals were kept entirely confidential, representing 4% of debt funding.

The disclosure patterns within debt deals have generally followed an upward trend over recent years. In 2023, the rate of fully disclosed debt deals rose to 78% (58 deals), a slight increase from 75% in 2022. This category of deals accounts for 89% of the total debt funding amounts, representing a significant concentration of funding in fully disclosed transactions.

Diving deeper into both fully and partially disclosed debt deals, together they account for 64 out of 74 transactions, which equates to 86% of the total number of debt deals. In terms of funding volume, these deals represent $1.16B, or 96% of the overall debt funding, underscoring the level of transparency in a majority of the debt deals in the market.

Conversely, confidential debt deals still play a role in the ecosystem: they represent 14% of the total number of debt deals, or 30 individual deals. Notably, these transactions are predominantly smaller in scale, which aligns with their contribution of only 4% to the total debt funding amount.

This distribution and evolution in the disclosure of debt deals provide insight into the prevailing disclosure trend of debt deals in the African tech venture capital sector, particularly in larger-scale funding rounds, while smaller, confidential deals continue to form a vital, yet smaller, part of the landscape.

SUBSCRIBE TO OUR NEWSLETTER